How National Borders and Capital Crises Are Reshaping the Satellite Industry

By Evan Grey Legal Contributor, SatNews

Editor’s Note: In this installment of his ongoing series on the regulatory landscape, Evan Grey moves beyond technical reporting to make a thesis argument about the operational consequences of new sovereign mandates. Grey contends that the policy shifts we’ve previously tracked are now triggering a lasting structural realignment of the satellite industry. You can find his previous analysis on the rise of spectrum protectionism here.

The End of Technical Neutrality

The commercial satellite communications sector has reached a structural turning point. The assumption of a borderless sky, where global mesh networks and technical neutrality defined market access, no longer holds. The industry has entered a new phase in which states intervene directly to enforce what amounts to orbital sovereignty. The low Earth orbit (LEO) market is no longer a global common.

It has fractured into at least three distinct spheres. China and Europe have moved to decouple from Western commercial dependencies, with the €10.6 billion SpaceRISE consortium now entering the final procurement phase of the European Union’s IRIS² program. This is not ordinary competition. It is a deliberate effort to build independent orbital infrastructure, motivated in large part by the strategic discomfort of relying on a single American provider.

Meanwhile, China has strengthened its position in spectrum coordination following the rapid succession of Long March 12 and 12A launches in December 2025 from commercial spaceports, accelerating the deployment of its state-backed megaconstellations. By successfully recording a coordinated batch of filings with the ITU for approximately 203,000 spacecraft, Beijing has secured priority spectrum rights and significant coordination leverage. The cost and complexity of coordination increase substantially for competitors, and China’s regulatory position gives it meaningful leverage in any negotiation over shared orbital resources.

Capital Structure Crisis: Spectrum Divestitures and Strategic Abandonment

The financial landscape is equally disruptive. EchoStar’s sale of its AWS-4 and H-block spectrum licenses to SpaceX, structured at approximately $17 billion in cash and stock with an additional $2 billion in interim debt servicing, is the centerpiece of a broader divestiture program that also includes $23 billion in spectrum sales to AT&T. The $19 billion total consideration for the SpaceX transaction actually exceeded analyst valuations, and for EchoStar founder Charlie Ergen, the combined $40 billion in spectrum dispositions represents the culmination of a decades-long arbitrage strategy.

Key Satellite Operator Debt Positions, 2026-2027

| Operator | Principal Due | Strategy | Status |

| EchoStar (DISH) | ~$2.0B current | Spectrum divestiture | Under FCC review (Docket 25-302) |

| SES | ~$1.2B | Intelsat integration | In progress |

| Eutelsat | ~$0.9B | LEO/GEO hybrid pivot | Operational |

With this influx of capital, the narrative surrounding EchoStar’s subsequent actions requires a paradigm shift. On Jan. 12, 2026, Crown Castle terminated its master lease agreement with DISH, alleging $3.5 billion in payment defaults. However, armed with its spectrum windfall, EchoStar is not a company starving for cash; rather, this alleged default represents a calculated, strategic abandonment of physical terrestrial infrastructure. The capital markets have realized that building border-bound physical networks is no longer economically viable.

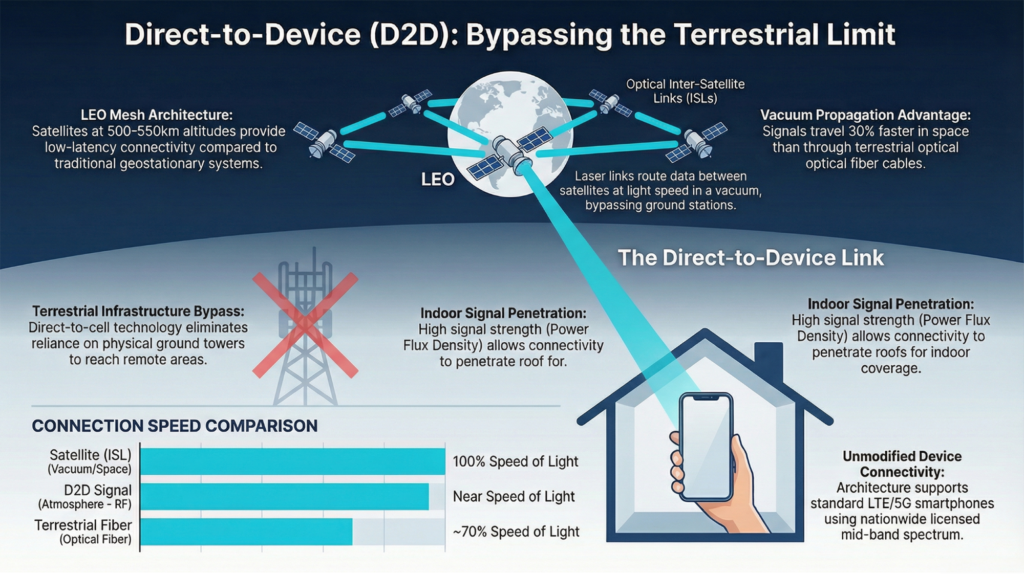

Direct to Device: The Regulatory Race

EchoStar’s exit from traditional terrestrial cell towers is not just a contract dispute—it is a white flag. If terrestrial economics are broken, the only solution is to put the tower in space. Consequently, the technical battleground for satellite connectivity has shifted decisively toward Direct to Device (D2D).

The FCC’s grant of the SpaceX and T-Mobile Supplemental Coverage from Space license on Dec. 16, 2025, was a landmark authorization. By permitting a power flux density (PFD) of -110.6 dBW, the Commission gave satellite operators the signal strength needed for indoor coverage, effectively overriding incumbent terrestrial operators’ interference objections.

AST SpaceMobile’s hardware ambitions tell a complementary but more uncertain story. The company’s BlueBird Block 2 satellites, which launched on Dec. 23, 2025, represent a different architectural bet: massive phased arrays designed to deliver broadband speeds projected at up to 120 Mbps directly to unmodified handsets.

The Launch Bottleneck

But shifting infrastructure to orbit triggers a brutal physical constraint: launch capacity. Massive phased arrays, like AST’s BlueBirds or Amazon Leo’s constellation, require heavy lift. The geopolitical push for sovereign networks means launch vehicles are now strategic chokepoints.

Amazon Leo, the company’s rebranded satellite broadband program, has encountered exactly this operational constraint. Despite opening a $140 million payload processing facility at Kennedy Space Center and completing six launches in 2025, the program has missed its early 2026 deployment targets. On Jan. 30, 2026, Amazon formally requested a 24-month extension from the FCC, disclosing that a “near-term shortage of available rockets” and required re-engineering had delayed its July 30, 2026, milestone. The dependency on Blue Origin’s New Glenn and ULA’s Vulcan has moved from a theoretical concern to a present bottleneck. In a striking display of this constraint, Amazon has been forced to book additional launches with SpaceX, its primary competitor, just to maintain its FCC license timeline.

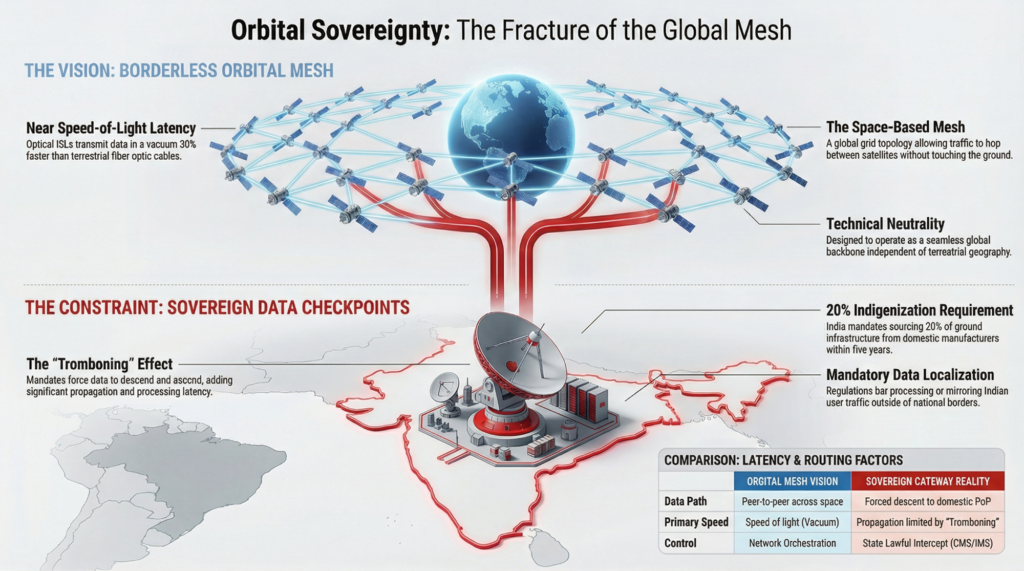

A Spectrum of Sovereignty: Gateways and Protectionism

Yet, even if an operator successfully navigates the capital shift, pioneers the D2D hardware, and survives the launch bottleneck, they crash into the final barrier: the sovereign checkpoint. Once in orbit, global mesh networks are being stripped of their efficiency by national regulators utilizing a diverse toolkit of sovereign enforcement.

In the Earth observation sector, the pivot to onboard AI processing, advanced by companies like Planet Labs and BlackSky, has successfully demonstrated that meaningful compute can happen in orbit. But the efficiency gains from decentralized orbital processing are being physically constrained by a parallel regulatory trend.

Regulators are asserting control through different means. India’s Department of Telecommunications enforces strict Data Sovereignty, requiring that data from LEO operators route through domestic ground infrastructure. Optical inter-satellite links (ISLs), the technology that allows constellations to route traffic across the mesh without touching the ground, become partly neutralized when regulators require every national data flow to pass through a sovereign gateway. Conversely, Brazil enforces Spectrum Protectionism; Anatel’s Resolution 772 regulatory framework forces new global LEO systems to yield to established, locally authorized satellite systems to prevent interference. Both tactics fundamentally alter the economics of constellation operation. Multiply these localized constraints across dozens of growth markets, and the cost model that justified global mesh architectures begins to erode.

The Operating Reality

The weight of evidence favors a structural reading. The convergence of independent forces—sovereign spectrum strategies, capital structure shifts, and mandatory ground infrastructure—is not a temporary alignment. Each reinforces the others.

The satellite sector is transitioning from a technology market into a compliance market. Technical superiority remains important, but it is increasingly secondary to regulatory access and financial durability. The EchoStar divestitures and the push for Direct to Device connectivity are adaptive responses to a world in which the borderless network is being physically re-architected to accommodate state sovereignty. The sky is not dead. Satellites are launching faster than ever. But it is a map of sovereign checkpoints, and operators who fail to read that map will not survive the next cycle.

About the Author

Evan Grey is a legal contributor for SatNews. A lawyer with a focus on regulatory policy and international relations, he specializes in the evolving geopolitical and industrial frameworks of the global space sector.